Why You're Bad With Money (And Why It's Not a Character Flaw)

Financial struggles aren't evidence of weakness. They're evidence of missing systems. Here's how to stop blaming yourself and start building structures that actually work.

You've tried. You've downloaded the apps, made the spreadsheets, promised yourself that this month would be different. And then it wasn't. Again.

So you conclude what feels obvious: you're bad with money. Irresponsible. Lacking discipline. Maybe you just weren't built for financial stability.

Here's what's actually true: the problem isn't your character. It's your system—or more accurately, the absence of one.

The Willpower Trap

Most financial advice assumes you'll remember to check your budget, resist impulse purchases through sheer determination, and manually transfer money into savings before you spend it elsewhere. This is asking you to fight your own brain every single day.

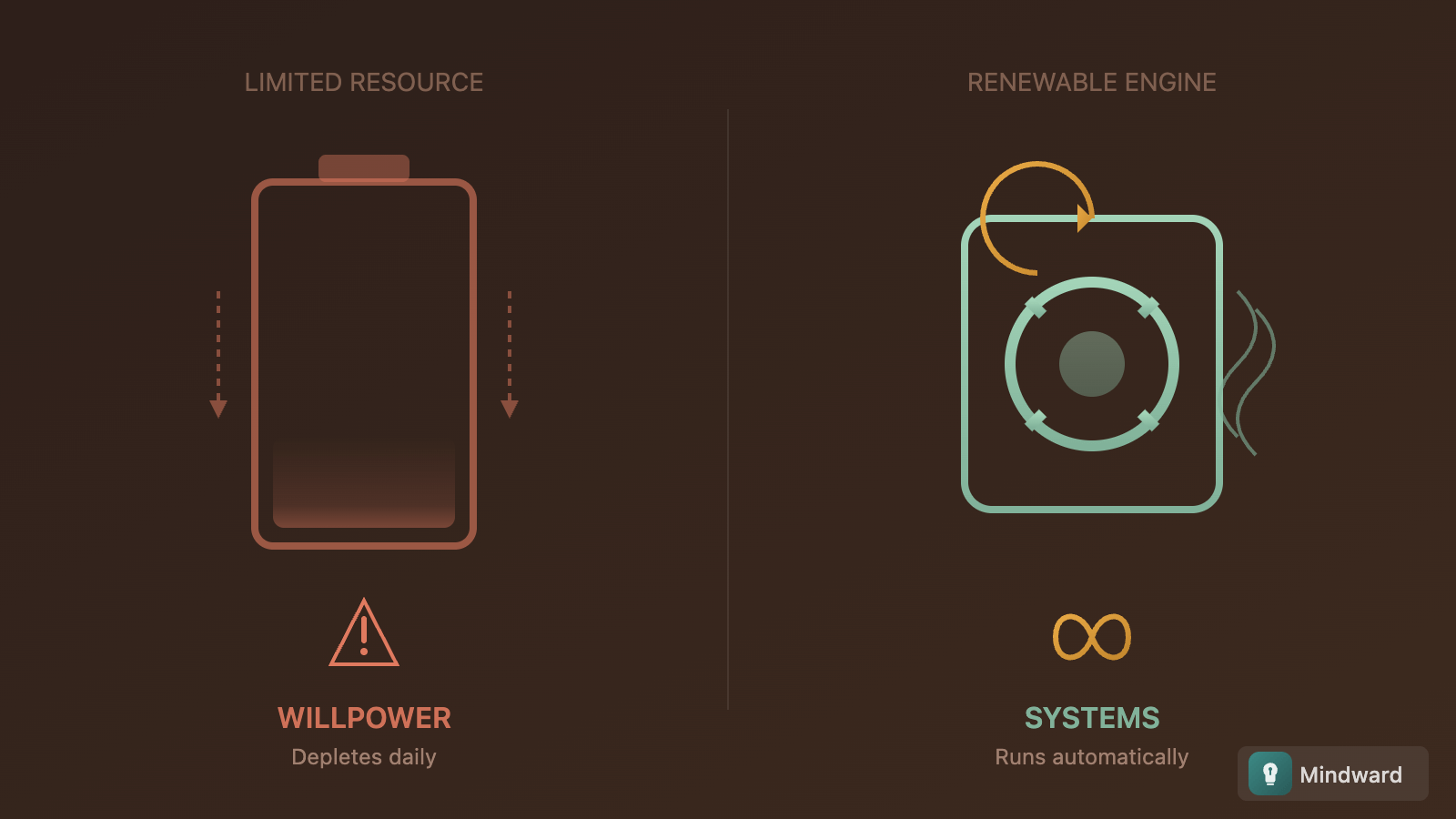

Willpower is a limited resource. It depletes throughout the day and crumbles under stress—exactly when financial decisions tend to get harder. Relying on willpower for money management is like relying on motivation to brush your teeth. It works until it doesn't, and then everything falls apart.

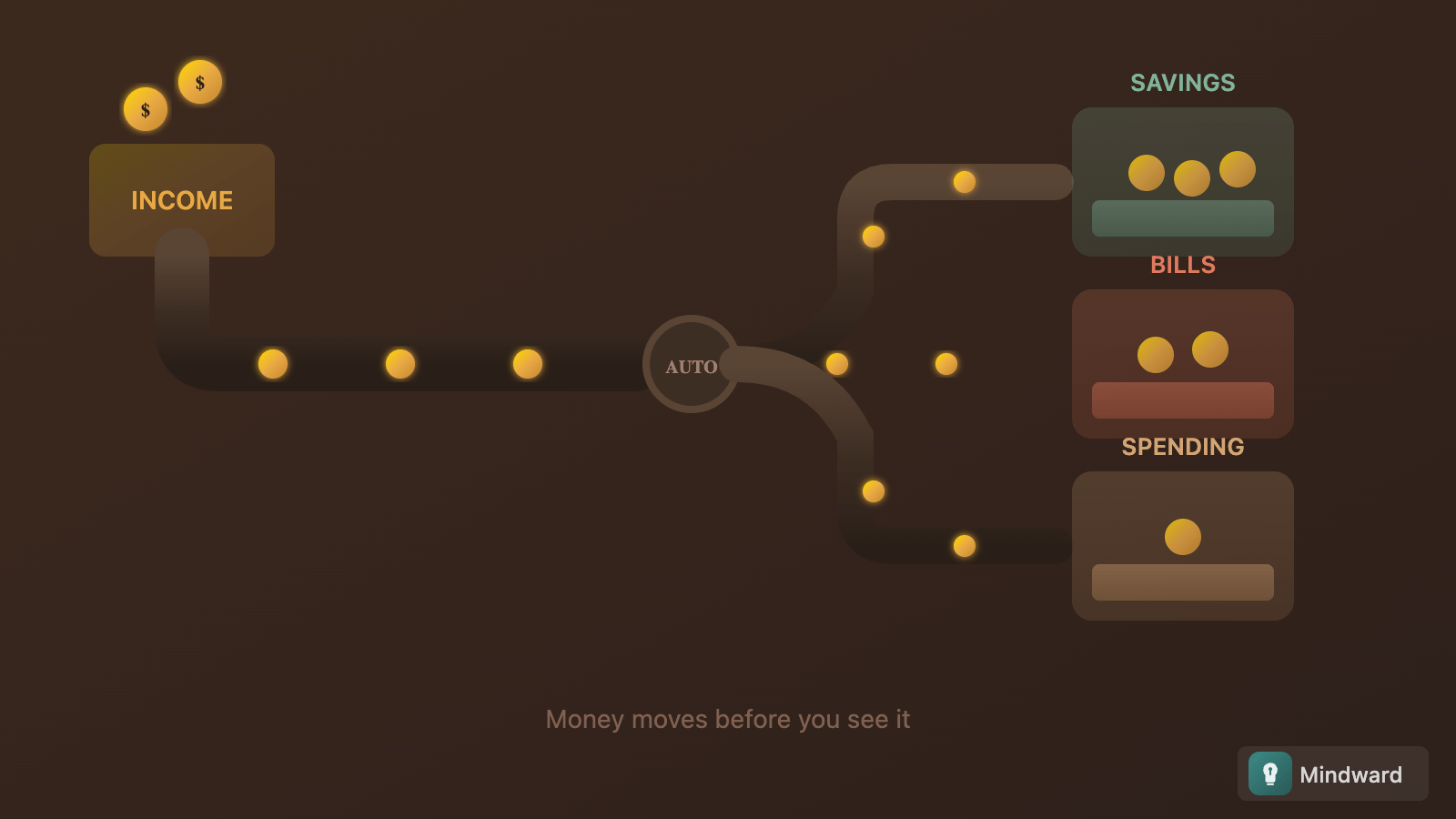

The people who appear "good with money" aren't exercising superhuman discipline. They've built systems that make the right choice the default choice. The money moves before they see it. The friction is placed in front of spending, not saving.

What's Actually Happening

When money hits your account and sits there, it's available. Available money gets spent—not because you're weak, but because that's what available money does. Every purchase feels like a small, reasonable decision in isolation. The problem is never one purchase. It's the accumulation of reasonable decisions that were never filtered through a larger intention.

This isn't a flaw. It's default human behavior. Your brain isn't wired to think in monthly aggregates or annual projections. It thinks in immediate context: I have money, here's something I want, this amount won't matter.

You're not bad with money. You're unprotected from your own defaults.

Systems Over Discipline

The shift isn't about trying harder. It's about designing an environment where trying isn't required.

Automatic transfers move money to savings before you can consider spending it. Separate accounts create psychological boundaries—money in your "bills" account doesn't feel available the way money in your main account does. Waiting periods on purchases introduce friction that filters out impulse from intention.

None of these require discipline in the moment. They require one decision upfront, and then they run in the background. The system does the work your willpower was never designed to do.

The Real Barrier

If systems are so effective, why doesn't everyone use them? Because building a system requires confronting reality first. You have to look at what you actually spend, not what you think you spend. You have to acknowledge the gap between your intentions and your behavior.

That confrontation feels like judgment. It triggers the same shame that made you conclude you were "bad with money" in the first place. So you avoid it, and the cycle continues.

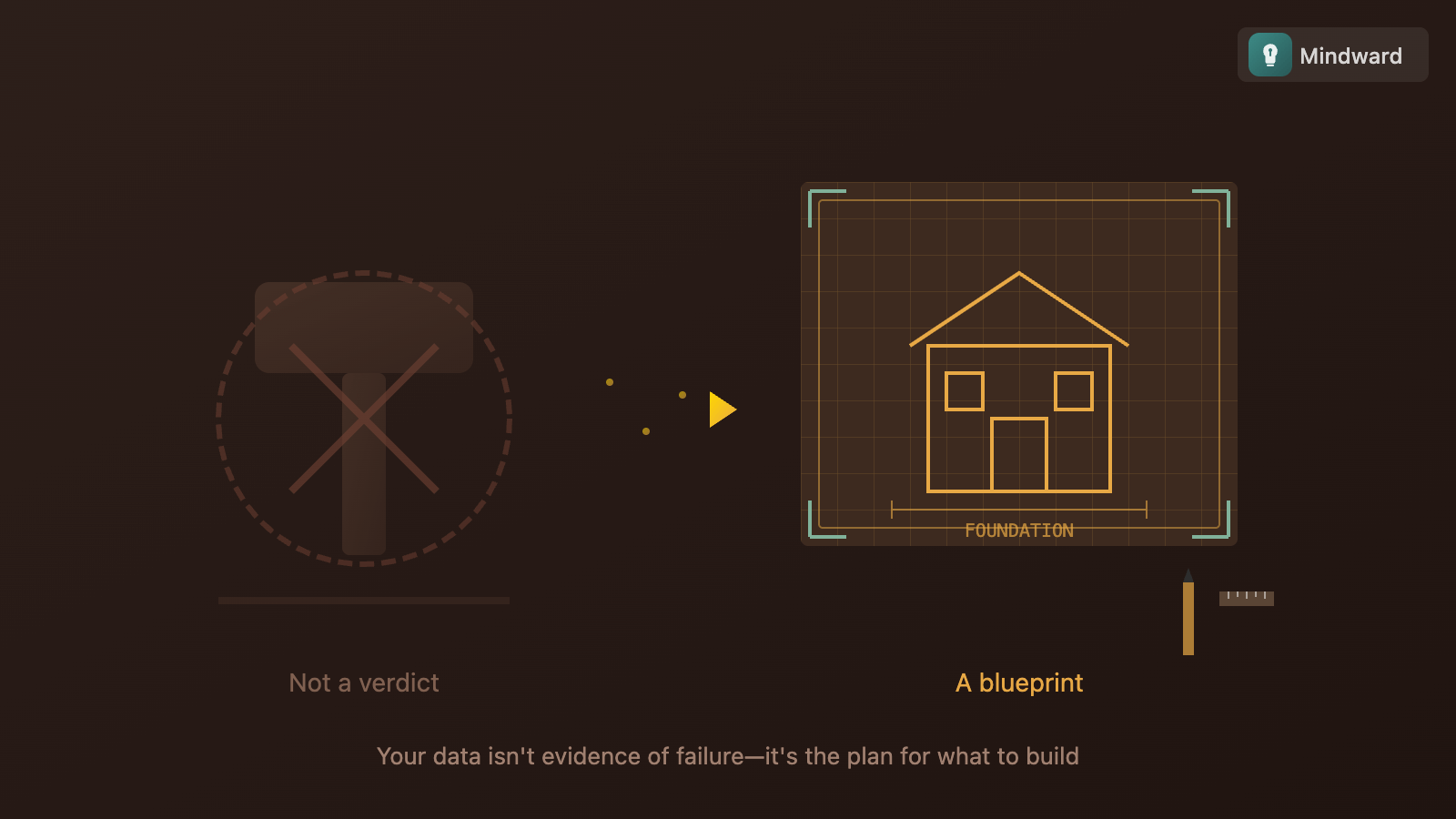

But here's the reframe: looking at your finances isn't collecting evidence of your failures. It's gathering information for your system. You can't automate what you haven't examined. The data isn't a verdict—it's a blueprint.

Start With One Automation

You don't need to overhaul everything at once. That's another willpower trap disguised as productivity.

Start with one automatic transfer. The day after your paycheck hits, move a fixed amount somewhere you won't see it daily. The number matters less than the automation. You're not saving money—you're building the muscle of letting systems work.

- Set the transfer for the day after payday, not the day of

- Choose an amount you won't immediately undo

- Use a separate bank if possible—distance creates friction

- Forget about it for three months before evaluating

Once that feels normal—and it will, faster than you expect—add another layer. Separate accounts for bills. A 24-hour rule on non-essential purchases over a certain amount. Each addition reduces the daily decisions you have to make.

Identity Follows Behavior

The goal isn't to become someone who's "good with money" through force of will. It's to build systems that produce the outcomes a financially stable person would have—and then let your identity catch up.

When your savings account grows without effort, you start to see yourself as someone who saves. When your bills are paid automatically and on time, you stop carrying the low-grade anxiety of potential overdrafts. The behavior creates the evidence, and the evidence reshapes the belief.

You don't need to fix yourself. You need to set up systems that protect you from the defaults that weren't working.

You were never bad with money. You were just asked to do something hard without the structures that make it manageable. Build the system, and let the system do what willpower couldn't.

Comments

How did you like this article?

No comments yet. Be the first to share your thoughts!