Why Budgets Fail (And What to Build Instead)

You've tried budgeting. It didn't stick. The problem isn't your discipline—it's the model itself. Here's what actually works when willpower won't.

You started the budget on a Sunday. By Wednesday, you'd already broken it. By the following month, you'd stopped opening the app entirely. And somewhere in the back of your mind, you filed it under 'things you're apparently not disciplined enough to do.'

But the budget didn't fail because you lack discipline. It failed because budgets are designed wrong. They ask you to make dozens of correct decisions every day, indefinitely, using a resource—willpower—that depletes with every use.

That's not a plan. That's a setup for failure.

The Willpower Problem

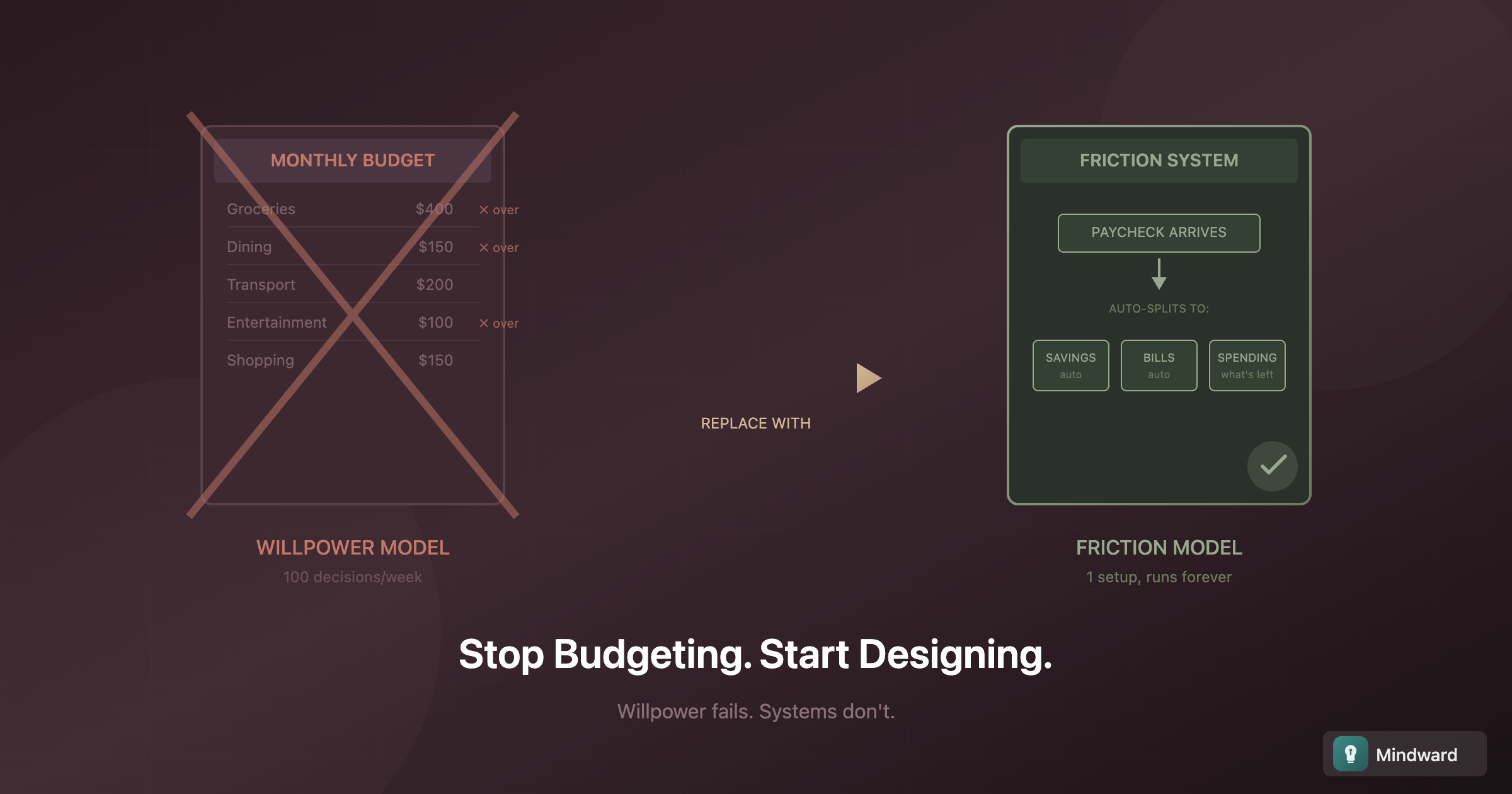

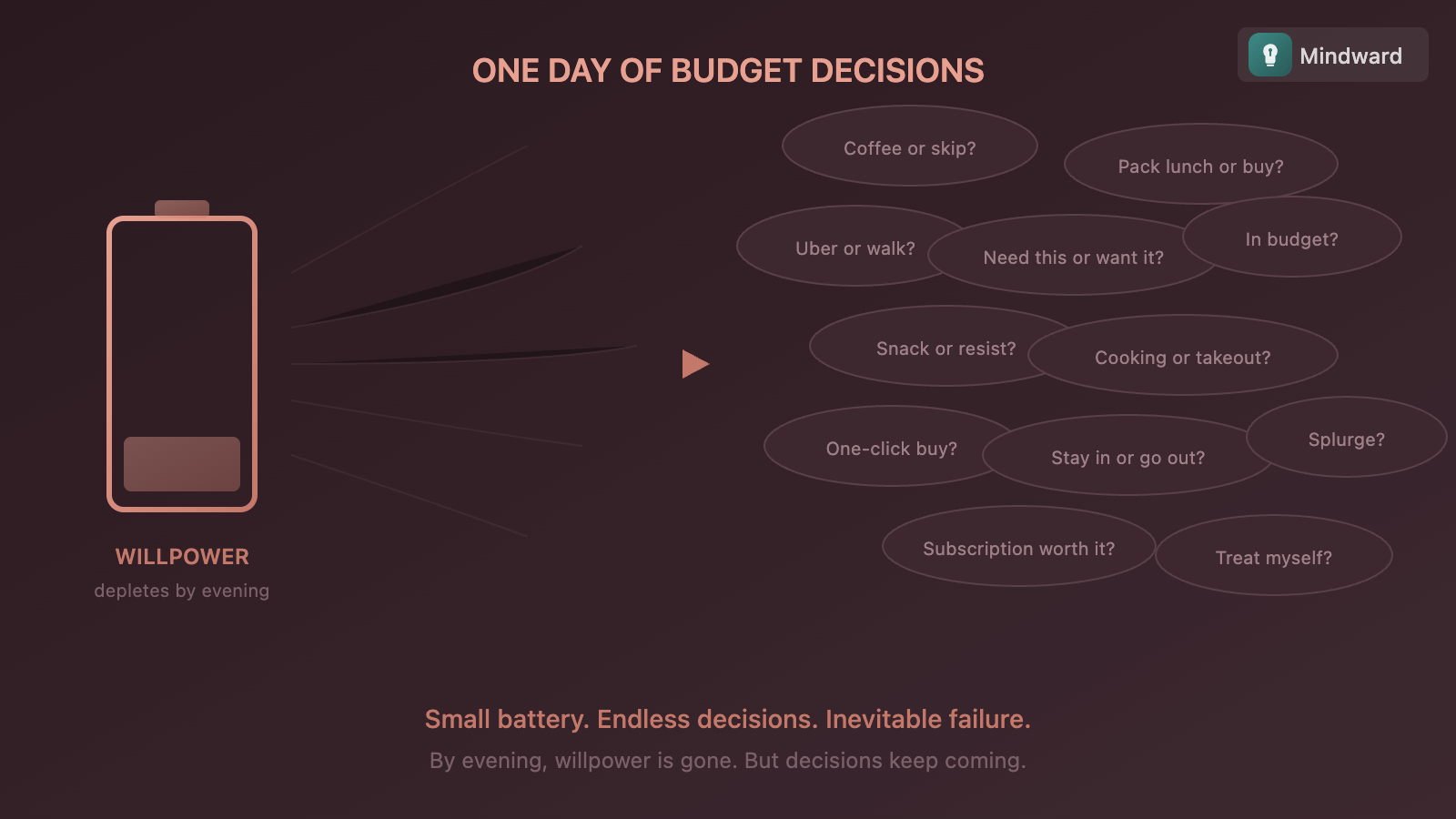

Traditional budgets work like this: you allocate money to categories, then use self-control to stay within those limits. Every purchase becomes a decision. Every decision requires effort. Every day, you're asked to choose correctly—at the grocery store, online at midnight, when you're stressed or tired or celebrating.

Willpower isn't infinite. It's a depletable resource that runs low by evening, collapses under stress, and recovers slowly. Building your entire financial system on willpower is like building a house on a foundation that dissolves in rain.

Every budget that requires daily discipline is already waiting to fail. The question is just when.

What Actually Works: Friction

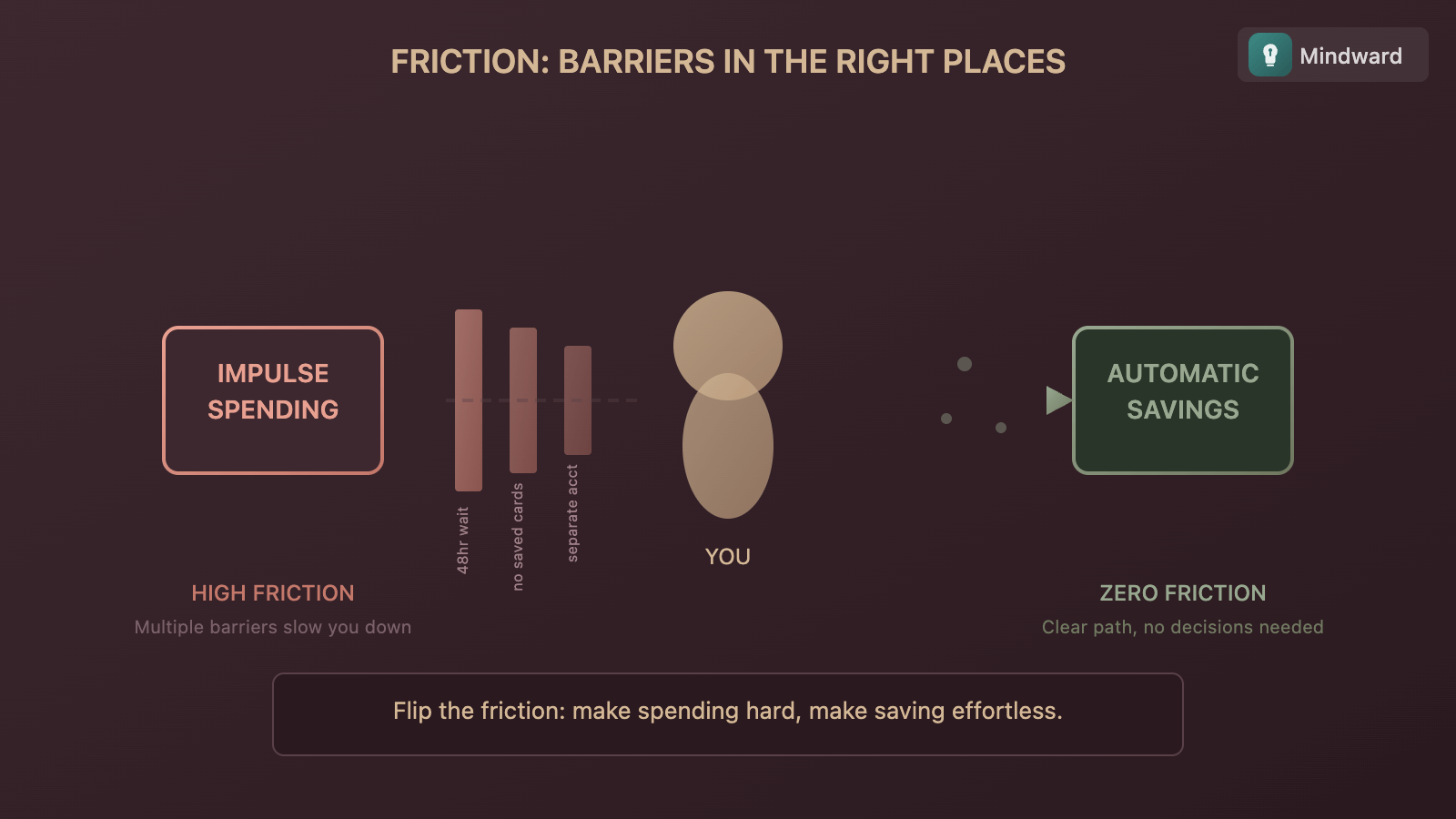

The alternative isn't more discipline. It's designing an environment where good decisions require less effort than bad ones. This is friction—the invisible force that makes some actions easier and others harder.

Right now, spending is frictionless. One click, one tap, one swipe. Saving requires effort—transferring money, checking balances, resisting what's available. The system is designed for spending, and you're fighting upstream.

Flip it. Make spending require effort. Make saving automatic. You're not relying on making good choices. You're making bad choices harder to make.

Building the Friction System

This isn't about restriction. It's about architecture. You're designing an environment where the path of least resistance leads somewhere useful.

- Automate first: Savings transfer the day after payday, before you see the money. What you don't see, you don't spend.

- Separate accounts: Bills in one account, spending in another. When the spending account is empty, you're done. No mental math required.

- Remove stored cards: Delete saved payment methods from shopping sites. The 30 seconds to find your wallet is often enough to stop impulse purchases.

- Implement waiting periods: Anything over $50 goes on a 48-hour list. Most items won't feel urgent after two days.

- Use cash for problem categories: Physical money creates natural friction. When it's gone, it's gone.

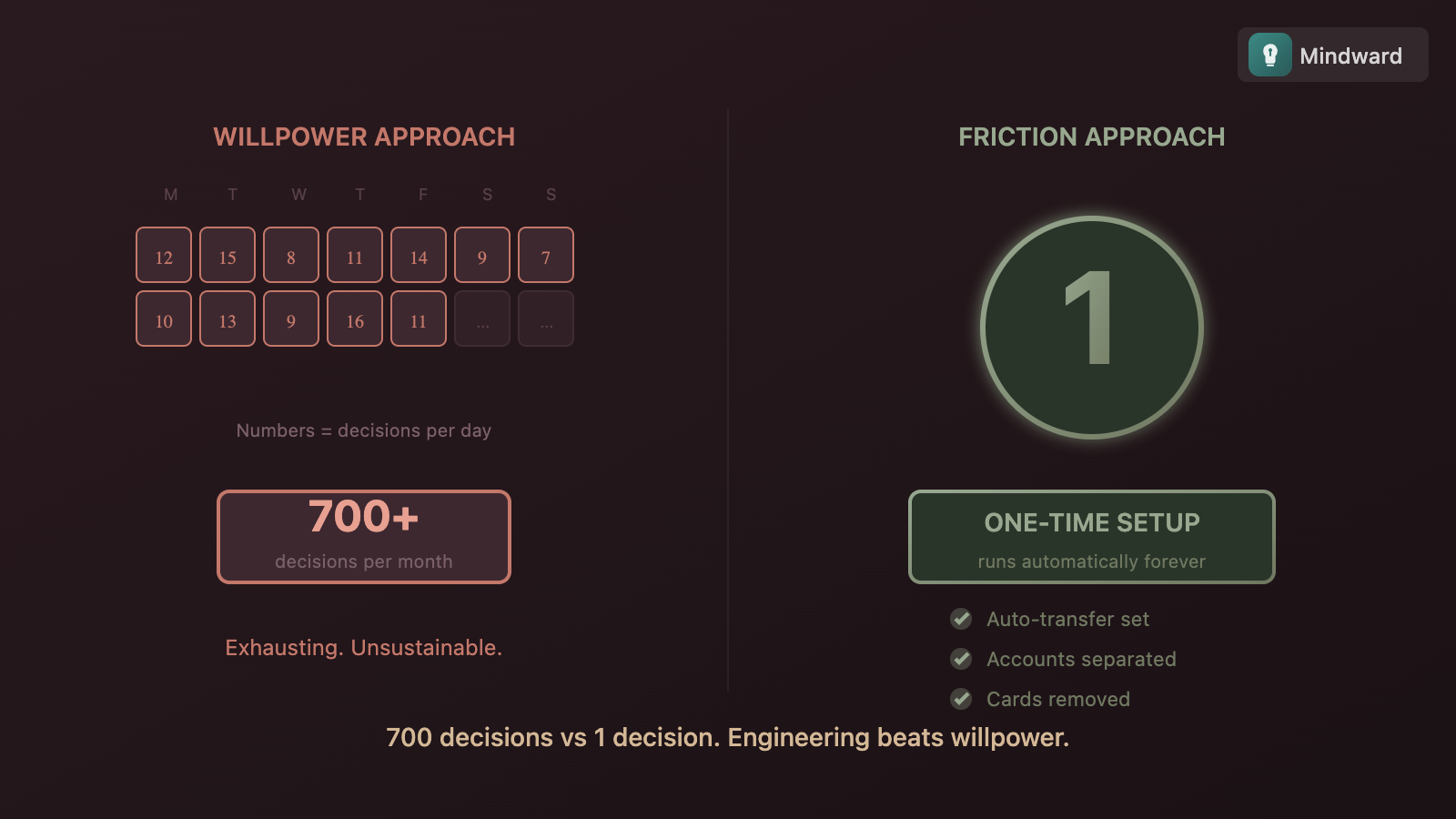

The One-Decision Advantage

Here's what changes: instead of making a hundred small decisions correctly every week, you make a few big decisions once—and then let the system run. Set up the automatic transfer. Create the separate accounts. Remove the stored cards. Done.

You're not budgeting anymore. You're engineering. And engineering beats willpower every time, because it doesn't depend on how you feel on any given Tuesday.

The best financial decisions are the ones you only have to make once.

When You Need a Budget

Budgets aren't useless—they're diagnostic. When your friction system isn't producing results, a temporary budget helps you see where the money actually goes. It's a flashlight, not a lifestyle.

Track for one month. Find the leaks. Adjust your friction accordingly. Then put the budget away. You don't need to live inside a spreadsheet. You need to know enough to design the right environment.

Permission to Stop Tracking

If your automated savings are hitting their targets and your bills are paid, you don't need to know exactly where every dollar went. The outcome is the proof. The system is working.

This is the permission most people need: you can stop tracking and still be financially responsible. You can ignore the apps and still make progress. You can design your way out of the discipline trap and never look back.

Budgets fail because they fight human nature. Friction systems work because they use it. Build the environment once, and let it do the work your willpower was never meant to do.

You don't need more discipline. You need better design.

Comments

How did you like this article?

No comments yet. Be the first to share your thoughts!